Managing personal finances can sometimes feel overwhelming, but it can be much more manageable with the right strategies and tools. Whether you’re looking to save for a vacation, buy a home, or simply make sure you have enough for retirement, effective financial management is key.

Some practical ways to take control of your money include:

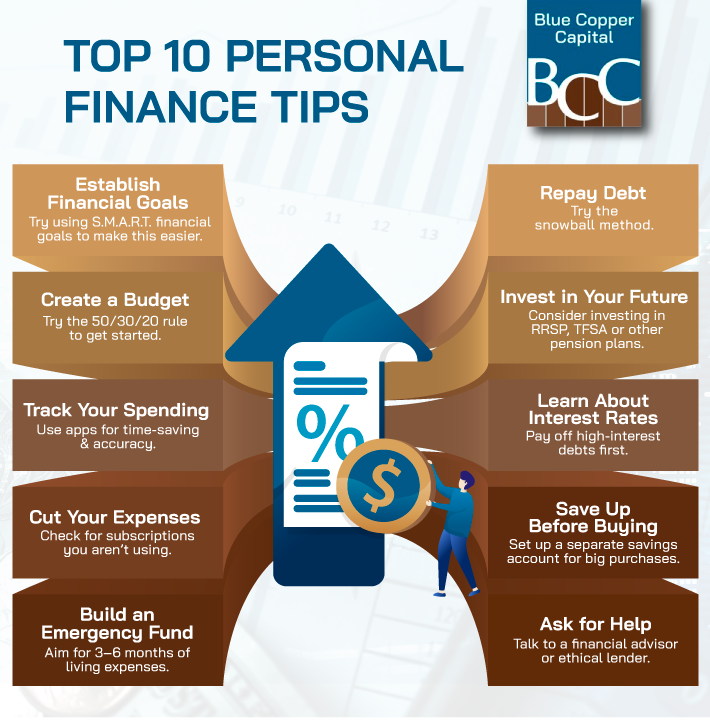

- Establishing financial goals

- Creating a budget

- Tracking your spending

- Cutting expenses

- Building an emergency fund

- Prioritizing debt repayment

- Investing

- Understanding interest rates

- Saving for big purchases

- Asking for help and guidance

Establish Financial Goals

Setting financial goals gives you direction and motivation. Using the S.M.A.R.T. framework is a great way to make sure your objectives are clear, actionable, and achievable.

How to Create S.M.A.R.T. Goals

- Specific: Clearly define what you want to achieve. Instead of saying, “I want to save money,” specify how much you want to save and for what purpose, like “I want to save $5,000 for a vacation.”

- Measurable: Make sure that your goal can be tracked. Establish milestones to monitor your progress, such as saving $500 each month until you reach your target.

- Achievable: Set realistic goals based on your current financial situation. Evaluate whether your aspirations are feasible and adjust if needed.

- Relevant: Align your goals with your overall financial objectives and life plans. For example, if buying a house is important, saving for a down payment should be prioritized.

- Time-bound: Assign a timeline for your goals to create a sense of urgency. Instead of simply wanting to save for a vacation, set a deadline, such as “I will save $5,000 by next July.”

Create a Budget

Creating a budget is the foundation of good financial management. Budgeting helps you understand where your money is going and live within your means.

There are a few different ways you can organize your budget, but regardless of the framework you choose, it just takes a few simple steps to get started:

- List your income: Include all sources of income, such as salary, freelance work, and investments.

- Track your expenses: Identify fixed expenses (rent, utilities) and variable expenses (groceries, entertainment).

- Set spending limits: Allocate specific amounts for each category to organize your spending.

- Review and adjust: Your budget will likely change over time as you get used to using it and create new habits or income streams. Regularly review your budget and make adjustments as needed.

Types of Budgets

Creating a budget is about setting realistic, achievable goals that help you succeed financially. The good news is that plenty of budget frameworks have already been developed to guide you.

Some popular choices include:

- The 50/30/20 rule: This divides income into 3 categories: 50 percent for needs, 30 percent for wants, and 20 percent for savings and debt repayment.

- The envelope system: This involves using physical envelopes for different spending categories. This can help curb overspending by limiting how much can be spent in each area.

- The zero-based budget: This allocates every dollar to specific expenses, savings, or debt repayment, making sure that income minus expenses equals zero at the end of the month. Companies often use this method, but it can be applied in a business or personal context.

Track Your Spending

Tracking your spending is essential to stay on budget. Consider using:

- Apps: Tools like Mint or YNAB (You Need A Budget) can automatically track your expenses.

- Spreadsheets: A simple Excel or Google Sheets document can also do the trick.

- Manual tracking: Keep receipts and note down expenses in a journal.

Knowing where your money goes helps you make informed financial decisions.

Cut Your Expenses

Reducing expenses doesn’t have to mean giving up what you love. Once you start tracking your spending, look for areas where you can cut unnecessary costs, like subscriptions you forgot to cancel. Small changes can add up to significant savings.

Other ways you might cut costs include:

- Eating out: Plan your meals in advance and try to make meals from scratch more. Food delivery orders can add up quickly. If possible, consider buying your essentials in bulk.

- Utilities: Use energy-efficient appliances and turn off lights when they’re not in use.

- Transportation: Use public transit, carpool, and take a walk or bike ride to change things up.

Build an Emergency Fund

An emergency fund acts as a financial safety net. Unexpected expenses, such as a car repair or medical bill, can throw off your budget and cause financial stress. A well-stocked emergency fund can help you weather these unexpected events without derailing your financial goals.

- How much to save: Aim for 3–6 months of living expenses.

- Where to keep it: Consider keeping your emergency fund in a high-yield savings account for easy access but with some interest earnings.

- Start small: Save a portion of each paycheck, even if it’s just a small amount.

Prioritize Debt Repayment

Paying off debt is crucial for long-term financial stability. High-interest debt, such as credit card debt, should be prioritized first. Consider using the snowball method, where you pay off the smallest debt first and then move on to the next one. You’ll gain momentum and motivation to tackle larger debts as each debt is paid off.

Debt consolidation can be an effective strategy for managing and paying off debt. This process involves combining multiple debts into a single loan, often with a lower interest rate.

This simplifies your financial obligations, as you’ll only have one payment to manage each month instead of several. Additionally, debt consolidation can help you reduce monthly payments and lower the total amount of interest you pay over time, making it easier to manage your finances.

Invest in Your Future

Investing can help grow your wealth over time and set you up for a comfortable future. Time is a powerful ally in retirement savings. Starting early allows you to benefit from compound interest. Even small, consistent contributions can accumulate significantly over time, so consider setting up automatic contributions to help you stay on track.

Some options for investing include:

- Registered retirement savings plan (RRSP): Contributing to an RRSP allows you to deduct contributions from your taxable income, reducing your overall tax burden during your working years. Investments within the RRSP grow tax-deferred until withdrawal, usually in retirement when you may be in a lower tax bracket.

- Tax-free savings account (TFSA): A TFSA offers the flexibility of tax-free growth and withdrawals. Contributions are not tax-deductible, but any earnings and withdrawals do not affect your taxable income. This makes it a great alternative for shorter-term goals, emergency funds, and retirement savings.

- Pension plans: If your employer offers a pension plan, be sure to understand its structure, whether defined benefit or defined contribution. Participating fully—especially if there’s matching—can significantly enhance your retirement savings.

Understand How Interest Rates Work

Interest rates play a crucial role in determining how much you ultimately pay on borrowed money. They can vary significantly depending on the type of loan, your credit score, and current market conditions. Understanding how these rates work can empower you to make informed financial decisions and potentially save you money over time.

Strategies to Pay Less Interest

- Increase your credit score: A higher credit score can qualify you for lower interest rates. Pay your bills on time, reduce credit card balances, and avoid taking on unnecessary debt.

- Refinance debt: Consider refinancing existing loans to secure more favourable interest rates. This can lower your monthly payments and reduce the overall interest you pay over the life of the loan.

- Make extra payments: If possible, make additional payments towards your loans, particularly on high-interest debt. This can reduce the principal balance sooner and save you money on interest in the long run.

Save Up for Big Purchases

It’s essential to save for significant expenses instead of relying on credit. Whether it’s a new car or a down payment on a house, saving in advance can help you avoid additional debt.

Consider setting up separate savings accounts for specific purchases so that you don’t have to use up other funds when the time comes to make them.

Ask for Help

Don’t hesitate to seek professional help. Financial advisors can offer personalized advice and help you create a solid financial plan. Additionally, if you’re struggling with debt, consider loan consolidation options to make repayments more manageable.

Start Working Toward Your Goals Today

Taking control of your personal finances is a continuous process, but the rewards are well worth the effort. Start implementing these tips today to build a more secure financial future.

If you need personalized advice or help managing debt, reach out to Blue Copper Capital for transparent guidance and support. We focus on understanding your financial situation and work collaboratively to develop personalized repayment plans that suit your budget.

Remember, successful financial management is within your reach. Begin today, and watch your financial health thrive.