Unlocking the benefits of a personal loan can be a game-changer. Whether you’re looking to consolidate debt, cover unexpected expenses, or fund a major purchase, understanding the key requirements before applying can save you time and make for a smoother process. Before applying for a personal loan, it is important to review the following requirements:

- Employment income

- Debt-to-income ratio

- Bank account information, such as your banking history and credit score

- Collateral

- Must be 18 years or older

Personal loans can offer a versatile financial solution, providing access to funds for various needs. Their appeal lies in their flexibility and straightforward application process, making them a popular choice for individuals seeking to manage their finances more effectively.

Types of Personal Loans

In Canada, there are 2 types of personal loans available.

Unsecured Term Loan

An unsecured term loan is a type of personal loan that doesn’t require any collateral. This means that you won’t need to pledge any assets like your home or car to secure the loan. Instead, the approval is based on your creditworthiness and ability to repay the loan.

Unsecured term loans are ideal for individuals with a good credit history and a stable income who need quick access to funds without risking their assets. They are commonly used to consolidate debt, cover medical expenses, or finance major purchases.

Pros & Cons

Pros:

- No collateral required, reducing risk to personal assets

- Faster approval process compared to secured loans

- Flexibility in the usage of funds

Cons:

- Higher interest rates due to increased risk for lenders

- Stricter credit requirements

- Lower loan amounts compared to secured loans

Secured Term Loan

A secured term loan requires collateral, meaning you must pledge an asset such as your home, car, or savings account to secure the loan. The collateral provides security for the lender, reducing their risk and often resulting in lower interest rates.

Secured term loans are suitable for individuals who may not have a strong credit history but have valuable assets they can use as collateral. These loans are often used for larger expenses like home improvements or starting a business.

Pros & Cons

Pros:

- Lower interest rates due to reduced lender risk

- Higher loan amounts available

- Easier approval for individuals with less-than-perfect credit

Cons:

- Risk of losing collateral if you default on the loan

- Longer approval process due to asset valuation

- Less flexibility in how to use the loan

What Is Required to Get a Loan?

Employment Income

Having a stable source of income is crucial when applying for a personal loan. Lenders need assurance that you have the means to repay the loan. Employment income demonstrates your financial stability and reliability.

Debt-to-Income Ratio

Your debt-to-income (DTI) ratio is a critical factor in determining loan eligibility. This ratio compares your monthly debt payments to your gross monthly income. A lower DTI ratio indicates better financial health and increases your chances of loan approval.

Bank Account Information

An active bank account with a positive banking history is essential. Lenders review your account activity to assess your financial behaviour. Additionally, a good credit score reflects your creditworthiness and can significantly impact loan approval and interest rates.

Collateral

If you’re applying for a secured loan, you’ll need to provide collateral. This could be any valuable asset like real estate, a vehicle, or savings. The collateral reduces the lender’s risk and can improve your loan terms.

Must Be 18 Years or Older

To apply for a personal loan, you must be at least 18 years old. This legal requirement makes sure that you are of legal age to enter into a financial contract.

Documents to Complete & Bring

In addition to the specified requirements, it is important to gather other supporting documents to prepare for a loan application.

Loan Application

The first step in the loan process is completing a loan application form. This form collects your personal information, financial details, and the purpose of the loan. While going through the loan application, take your time and make sure all information is accurate and complete.

Proof of Identification

You’ll need to provide valid identification, such as a driver’s license, passport, or government-issued ID. This verifies your identity for compliance with legal requirements.

Employer & Income Verification

Lenders require proof of employment and income to assess your ability to repay the loan. This can include recent pay stubs, tax returns, or a letter from your employer.

Proof of Address

Proof of address is necessary to confirm your residence. Acceptable documents include utility bills, lease agreements, or bank statements showing your current address.

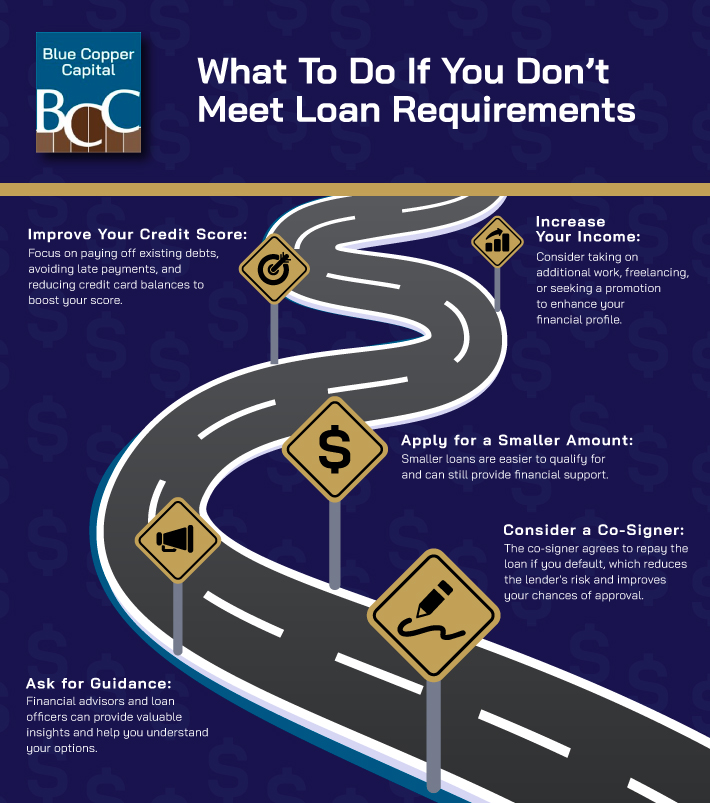

What to Do if You Don’t Meet Loan Requirements

Ask for Guidance

If you’re unsure about the loan requirements or need assistance, don’t hesitate to ask for guidance. Financial advisors and loan officers can provide valuable insights and help you understand your options.

Improve Your Credit Score

A higher credit score can significantly improve your chances of loan approval. Focus on paying off existing debts, avoiding late payments, and reducing credit card balances to boost your score.

Increase Your Income

Increasing your income can positively impact your loan eligibility. Consider taking on additional work, freelancing, or seeking a promotion to enhance your financial profile.

Apply for a Smaller Amount

If you don’t meet the requirements for a larger loan, consider applying for a smaller amount. Smaller loans are easier to qualify for and can still provide financial support.

Consider a Co-Signer

A co-signer with a strong credit profile can help you secure a loan. The co-signer agrees to repay the loan if you default, reducing the lender’s risk and improving your approval chances.

The Bottom Line

Navigating the personal loan landscape can be daunting, but understanding the key requirements and preparing accordingly can set you up for success. From identifying the right type of loan to gathering the necessary documents and improving your financial profile, each step brings you closer to securing the funds you need.

Remember, personal loans are a powerful financial tool when used responsibly. If you have any questions or need further assistance, don’t hesitate to contact Blue Copper Capital. Our team is here to help you every step of the way.