If you have poor credit, it can be a daunting task trying to figure out the best way to get back on track. Poor credit not only makes it difficult to secure a loan or open new lines of credit but can also limit your options when it comes to housing, transportation, insurance, and even employment opportunities.

The good news is there are a variety of ways you can improve your credit and get your financial goals back on track. From debt consolidation to improving your financial literacy, understanding how your credit score works—and what factors can lower it—can help you avoid the consequences of poor credit.

What Causes Poor Credit?

Your credit score is a reflection of your financial history, providing insight into your borrowing habits and how likely you are to repay loans and bills on time. Some of the main factors that affect your credit score are your payment history, credit utilization ratio, and the length of your credit history. A poor credit score may be caused by a variety of factors, including:

- Late or Missed Payments: One of the biggest contributors to bad credit is failing to make payments on time. Whether it’s a credit card bill, a loan repayment, or another financial obligation, consistently missing due dates will have a negative impact on your credit score.

- High Credit Utilization: Using too much of your available credit can signal financial instability to lenders. If you’re constantly maxing out your credit cards or carrying high balances, it can lower your credit score and make it harder to qualify for new credit.

- Defaulting on Loans: When you stop making payments on a loan altogether, it’s considered a default. Defaulting on a loan not only damages your credit score but can also put you at risk of legal action from the lender.

- Bankruptcy: Filing for bankruptcy is a last resort for many individuals facing overwhelming debt. While it offers a fresh start, it also leaves a lasting impact on your credit history. Bankruptcy can stay on your credit report for up to 7 years, making it challenging to rebuild your credit during that time.

- Lack of Credit History: Not having a credit history can also negatively affect your credit score. Lenders want to see a track record of responsible borrowing and repayment. If you have little to no credit history, it can make it harder to get approved for credit.

What Happens if You Have a Poor Credit Score?

Having a poor credit score can have significant consequences that affect various aspects of your life, from affecting your ability to be approved for loans to causing financial and emotional stress in your daily life.

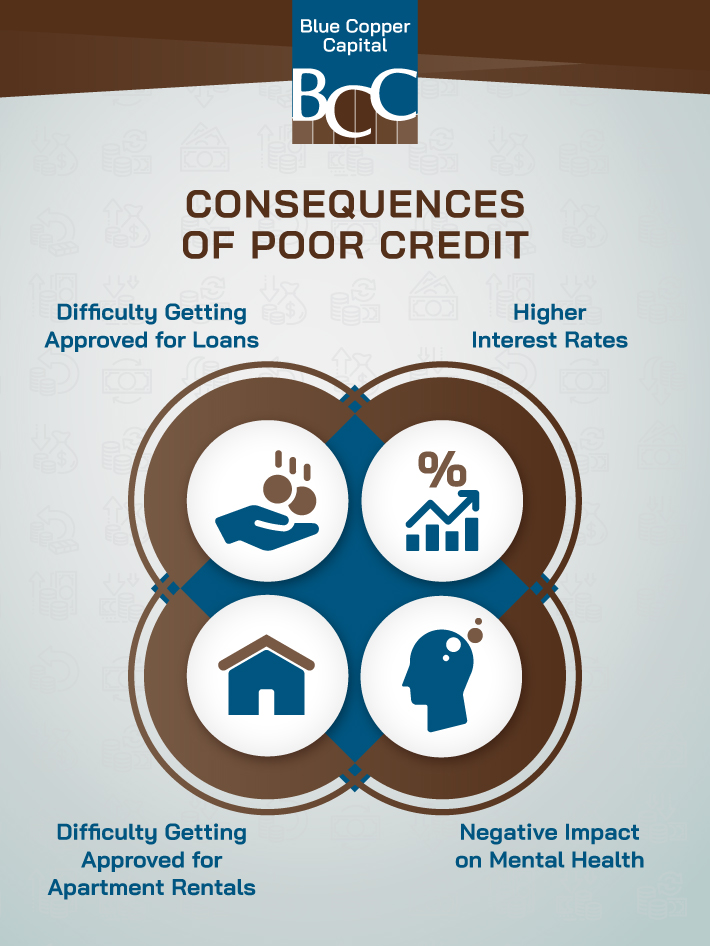

Difficulty Getting Approved for Loans

One of the biggest consequences of poor credit is the difficulty of getting approved for loans. Whether it’s a mortgage, car loan, or personal loan, lenders tend to view those with low credit scores as high-risk borrowers. This means you’re more likely to be turned down for loans and may have a harder time finding someone to lend you money.

Higher Interest Rates

If you are able to get approved for a loan with a poor credit score, the interest rates may be higher than if you have good credit. Lenders tend to charge higher interest rates to compensate for the added risk of lending to those with low credit scores. The costs of higher interest rates can add up over time and make paying off debt more difficult.

Difficulty Getting Approved for Apartment Rentals

Landlords and property management companies will often check your credit score before allowing you to rent an apartment or home. If you have a low credit score or a history of missed payments, you may have difficulty getting approved for a rental. A landlord may ask for higher upfront payments or a co-signer, making it more difficult to find a home to rent.

Difficulty Finding Employment

Another consequence of poor credit scores is the potential difficulty of finding employment. Some employers may check credit scores when considering job candidates, especially for positions that involve handling money. If you have a poor credit score, you may be viewed negatively by potential employers, which could limit your job opportunities.

Potential Negative Impact on Mental Health

Poor credit scores can also have a negative impact on your mental health. Constantly worrying about how to pay bills, dealing with collection calls, and living paycheck to paycheck can cause stress and anxiety.

How to Rebuild Your Credit Score

Having a poor credit score can have a significant impact on your daily life and financial well-being. Understanding the consequences of poor credit can help you take steps to improve your credit score and avoid these issues.

By making payments on time, paying off debt, and keeping credit usage low, you can improve your credit score and regain control of your finances. Rebuilding your credit score might feel overwhelming at first, but it can be done. With each small step you take, you’re moving closer to a brighter financial future. It may take time, but the benefits of a good credit score are worth the effort.

Financial Resources to Help You Maintain Good Credit

Being aware of the factors that affect your credit score can help you maintain good credit and avoid the pitfalls that come with having a poor credit score.

If you’re facing financial stress and are concerned about your ability to keep up with payments, reach out to our experienced team at Blue Copper Capital to learn more about your options.