If you have a credit history that isn’t ideal or you have a low credit score, you might find it difficult to get a personal loan, but bad credit doesn’t have to stand in the way of borrowing money.

To get access to the credit you need, there are many lenders that will assess more factors than just your credit score.

At Blue Copper Capital, we understand that getting a loan with bad credit can be a difficult thing to understand, and we’re here to help you through the process. Keep reading to learn more about different types of loans and how to apply for a loan if you have a bad credit score.

What is a Credit Score?

A credit score is a number based on an analysis of your credit report that represents how creditworthy you are. If you’re interested in getting a loan or taking out a line of credit, lenders can use this information to help the risk involved with lending you money.

Is My Credit Score Bad?

It’s important to check your credit score to see if you’re in good standing. Depending on which company you order your credit report and score from, you may be charged a fee.

Once you obtain your credit score, you can compare it to this breakdown of credit scores ranges in Canada:

- Excellent credit: A score of 741 to 900

- Good credit: A score of 713 to 740

- Fair credit: A score of 660 to 712

- Below average: A score of 575 to 659

- Bad credit: A score of 300 to 574

What Affects my Credit Score?

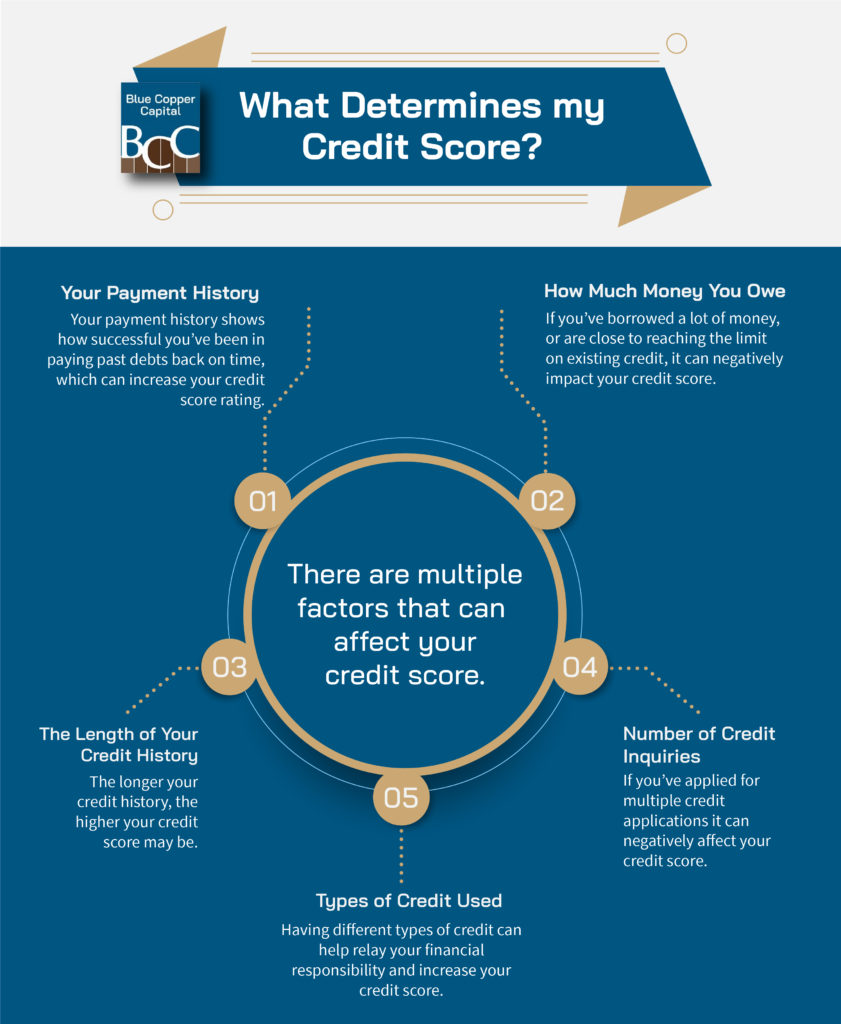

There are 5 main factors that determine your credit score.

Your Payment History

Your payment history is one of the most important factors in your credit score.

Your payment history is a collection of all the payments you’ve made against outstanding debts to date. If your payment history shows that you always pay your debts back on time, it increases your credit score rating. On the other hand, if you have a history of making late payments, or still have outstanding payments that are past due, it can negatively impact your credit score.

How Much Money You Owe

The amount of money you owe and your available credit can greatly impact your credit score. If you’ve borrowed a lot of money, lenders will take this amount into account for how much additional debt you can take on. Additionally, how close you are to reaching the limit on any existing credit you have can negatively impact your credit score.

The Length of Your Credit History

The longer your credit history, the easier it is for lenders to determine the likelihood of you paying back borrowed money on time.

Number of Credit Inquiries

If you’ve applied for multiple credit applications it can negatively affect your credit score as it may be a sign that you’re having financial difficulty. Sometimes, this can also include how many times you’ve checked your credit score in a set period of time.

Types of Credit Used

Having different types of credit helps demonstrate your ability to manage your financial responsibilities.

There are three main types of credit:

- Revolving credit is one of the most common types of credit. Revolving credit typically refers to a credit card from which you can borrow freely but has a limit, requires monthly payments, and involves interest charges on any owing balances.

- Installment credit refers to a loan for a set amount of money with a fixed, regularly occurring repayment schedule. This type of credit typically includes student loans, mortgages, auto loans, and personal loans.

- Open credit is less common, and you may not even see it on your credit report. Open credit refers to accounts that you can borrow from up to a maximum amount but which must also be paid back in full each month.

What is a Bad Credit Loan?

A bad credit loan refers to a type of loan that can help you borrow money even if you have a less than ideal credit score.

Depending on what you need a loan for, you generally have four options:

How Do I Get a Loan if I Have Bad Credit?

If you have bad credit, it might be reassuring to know that credit checks aren’t always the sole determiner of your eligibility to take out a loan.

If you have bad credit, discuss your options with your lender. Your lender can discuss other factors they can check to approve you for a loan, including:

- Your employment history & whether or not you’ve had a steady job

- Your annual income

- Your liquid assets including stocks, bonds, & any valuable property

- Your education level

- Your address history

- Any professional licenses that you may hold

Take the First Step

Every lender has a different process for determining risk, so it’s best to ask a lender directly for the factors they look at when assessing your eligibility.

If you have questions about your credit score, your borrowing eligibility, or anything else please don’t hesitate to reach out to our team at Blue Copper Capital.