“Recession” is a financial term you need to know, whether you’re a business owner or managing personal funds. When you’re unprepared for a recession, it can severely change your financial plans. During the 2020 recession or Great Lockdown, many businesses filed for bankruptcy, and individuals filed consumer proposals because of overwhelming debt.

About 48% of Canadians say they’ve lost sleep because of financial worries. But having a strategy can help you let go of financial stress and start planning for financial success.

Most recessions have warning signs, meaning changes won’t happen overnight. However, you can prepare for future recessions by strengthening funds and finances today.

What Is a Recession?

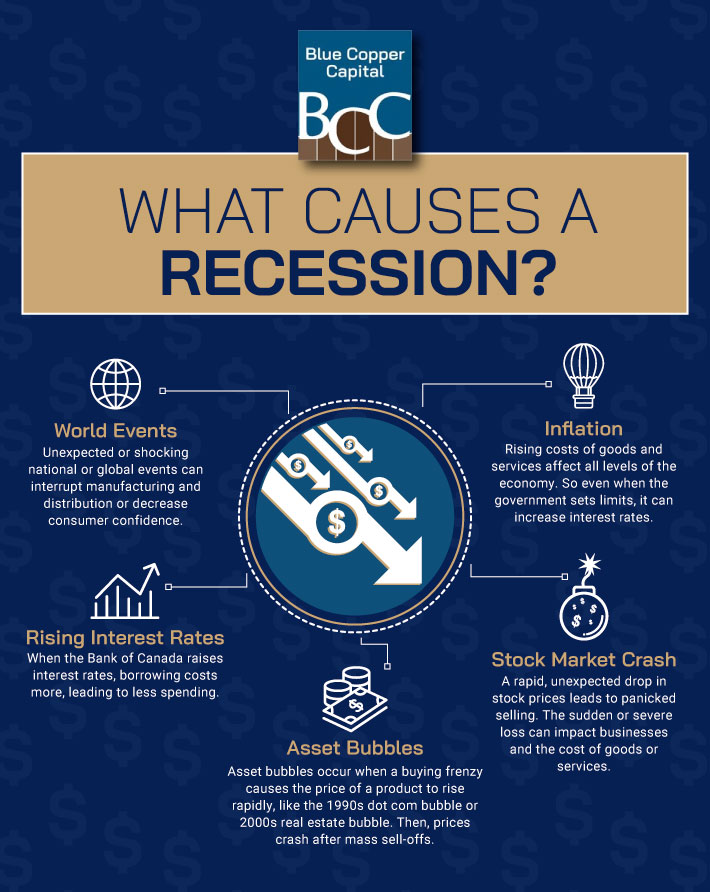

The basic recession definition is a short to medium period of economic decline, often having national or global impacts. Recessions can be caused by world events, high inflation, drastic unemployment rates, or stock market crashes.

The COVID-19 pandemic and the Ukraine-Russia war are prime modern examples of how global events can trigger a recession. With the pandemic, many manufacturers and businesses closed, preventing the production or delivery of goods and services. Likewise, the Ukraine-Russian war economic fallout (particularly the disruption of the supply chain for auto parts, oil, and grain) has increased consumer costs worldwide.

Canada ranked 4th highest for pandemic-relief spending among G20 countries, with a higher proportion than 11 other countries. The amount was equal to 12.3% of Canada’s gross domestic product (GDP) in 2020.

Generally, Canadians have more money in their pockets following the pandemic, which may inspire because of renewed access to services. But unfortunately, even with the Bank of Canada limiting interest rates, the interrupted supply chains led to inflation—with Canadians paying higher prices for fewer goods.

How Long Do Recessions Last?

On average, recessions last between 10–17 months. However, recessions can (rarely) happen back-to-back. A double-dip recession occurs when the economy experiences a decline, briefly begins recovery, and then drops into another recession.

The current economic climate shows initial signs of a double dip recession due to climbing inflation. But a stronger indicator is a negative GDP back-to-back.

Strategies for a Recession

Knowing how to prepare for a recession can help you survive or even experience success, no matter how long a recession lasts.

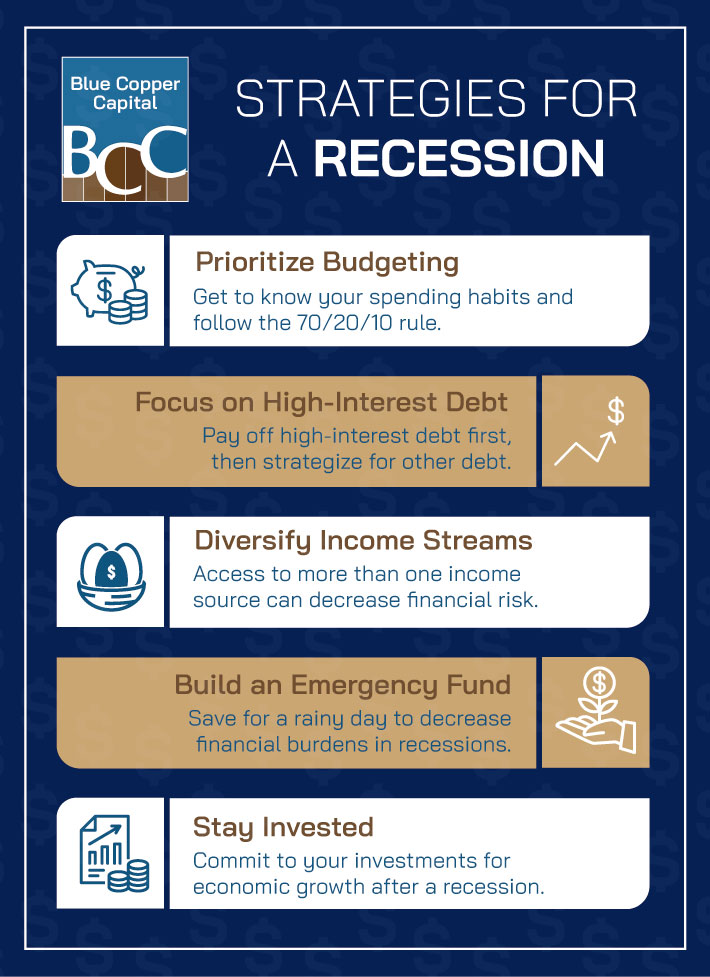

Focus on High-Interest Debt

Firstly, focus on paying off high-interest debt, particularly variable-rate debt. It may already be a priority, but it can be especially crucial when preparing for a recession. By having a clear strategy in place or starting the process now, you have an increased chance of building cash reserves for when you need it most. You may need future capital to invest or secure your savings.

Credit cards, personal loans, and mortgages can have variable interest rates. In times of economic stability, the appeal is a lower rate. Unfortunately, the rates can vary or climb during a recession, such as how mortgage rates ranged from 0.5% to 4.75% between 2005–2015.

Need tips on how to repay your loans faster? Changing your payment schedule, refinancing, or boosting your income are some possibilities. For example, you may find a lower interest rate with a line of credit or personal loan, allowing you to pay off a variable-rate debt.

Focus on Budgeting

Budgets are a staple of personal and professional financial planning. Knowing how you spend your money can help you meet your goals, whether growing your business or recovering from a financial loss.

The 70/20/10 rule for budgeting is a practical guideline for dividing a paycheque:

- 70% expenses (fixed & variable)

- 20% savings & investments

- 10% paying off debt or giving

Diversify Income Streams

How a future economic downturn will impact your income can be unpredictable. Recessions often lead to investment changes or job loss. Putting all your eggs in the same basket risks losing all your eggs when the recession hits. Having more than one income stream can help strengthen your financial standing.

Investments or entrepreneurial ventures can add passive income. Or, consider starting a side hustle or part-time job for extra active income. A diverse portfolio can help recession-proof your finances or add an option for emergency savings.

Build an Emergency Fund

Building an emergency fund means you have extra money for a rainy day. The rainy day might be the next Great Depression or your retirement. Creating a fund you can turn to in times of economic downturn or income loss can significantly decrease financial burdens.

The sooner you begin an emergency fund, the more flexibility you have to contribute. First, look at your budget and strategize the amount you’d need in your fund. Then, plan the fine details, like how much you need to contribute over what timeline.

Stay Invested

When warning signs signal an oncoming recession, your first instinct might be to reduce investments or pull out completely. However, recessions are typically followed by economic growth—meaning hanging in there can be rewarding long term.

When you prepare for a recession, you have more freedom to move forward with financial goals. Investing is also one way to diversify your income. The key is to make a plan and commit to it, even when investments go down before they go up.

Risk is associated with all forms of investments. Still, you can lower your risk by choosing stocks or products more likely to remain stable or increase during economic upheavals. For example, the consumer staples or healthcare sector will likely remain robust under most conditions.

Keep Living Your Life

The idea of a recession can seem daunting, but recessions are a normal part of economic cycles. Canada has experienced 5 recessions since the 1970s.

Change is the only constant, and economic ups and downs are expected. Planning for fair and stormy weather alike can turn downturns into opportunities. Getting prepared for the next recession today can make it easier to meet your financial goals regardless of what life throws at you.Whatever your financial goals, you deserve personalized attention to achieve success. At Blue Copper Capital, our mission is to help all clients reach their goals regardless of circumstances. Contact us today for your loan needs so you can start planning for your financial future.