For first-time car buyers or those trying to stay within a budget, the decision to lease or finance a car can be overwhelming. Each option has advantages and disadvantages, and the right choice depends on your financial situation, lifestyle, and long-term goals.

For many, financing a car is more appealing since it means you will own your vehicle outright. However, for those who want a shorter-term commitment and want to pay less outright, leasing might be a better fit.

Leasing a Car: The Pros

When you lease a car, you’re essentially renting it from the dealership for a predetermined period, usually 2–4 years. Leasing can be an attractive option for many reasons.

Lower Monthly Payments

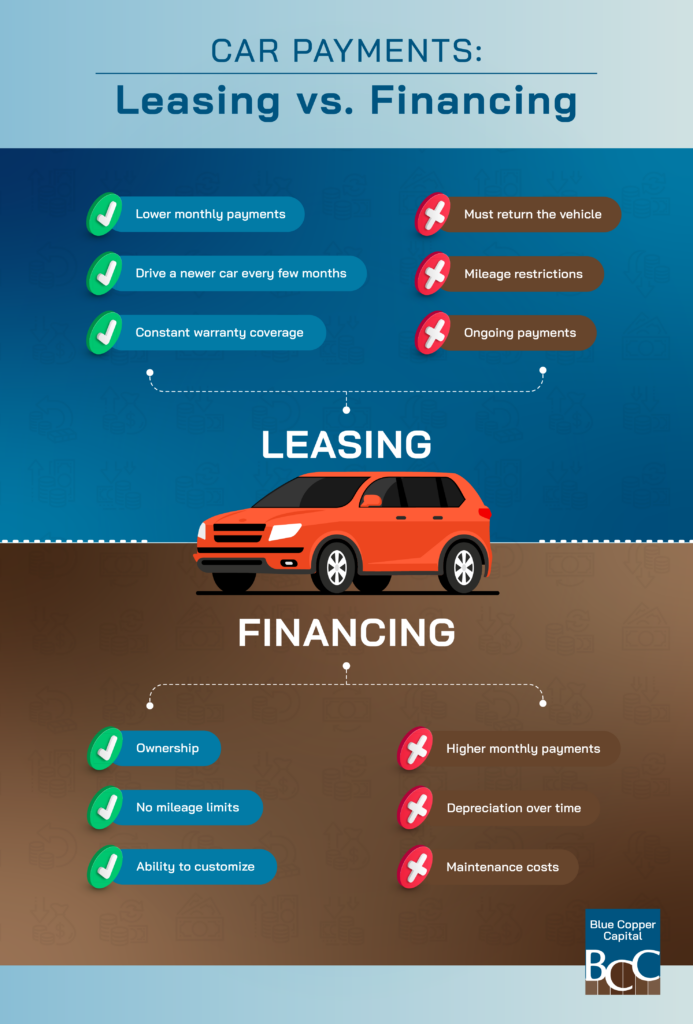

Leasing generally offers lower payments compared to financing. Since you’re only paying for the depreciation of the car during the lease term—not the full value of the vehicle—your average monthly payment tends to be less. For budget-conscious consumers, this can free up funds for other expenses.

Drive a Newer Car Every Few Years

One major advantage of leasing is the ability to drive a new car every few years. For those who love having access to the latest models, upgraded features, and improved technology, leasing is a smart way to do so without committing to a long-term purchase.

Warranty Coverage

Leased cars typically remain under warranty throughout the lease period, which means most repair costs are covered. This can make leasing more predictable and less financially stressful for those concerned about unexpected expenses.

Leasing a Car: The Cons

While leasing has its perks, it’s important to weigh the drawbacks before making a decision.

Mileage Restrictions

Most leases come with mileage limits, usually between 16,000 and 20,000 kilometres per year. Exceeding those limits often results in hefty penalties. If you have unpredictable driving patterns or regularly take long trips, this limitation can be a dealbreaker.

No Ownership

At the end of a lease, you don’t own the car. If you enjoy the idea of building equity in a vehicle or eventually having a car payment-free period, leasing may not be for you.

Ongoing Payments

Since you don’t own the vehicle, there’s no way to eliminate payments unless you choose to purchase a car afterward. This creates a cycle of ongoing payments with little return on your investment.

Financing a Car: The Pros

Financing a car means taking out a loan to buy the vehicle, eventually making it your own. For some, this makes it a more appealing option.

Ownership

When you finance a vehicle, you’ll ultimately own it once the loan is paid off. For many, this is the most appealing element of financing a car, as it represents a tangible asset you can keep, sell, or trade-in as you see fit. Successfully paying off your car loan can also give you a sense of financial freedom and flexibility.

No Mileage Limits

Financing gives you unlimited freedom to drive without restrictions. If you travel extensively or have unpredictable driving patterns, this benefit ensures you’ll never have to worry about penalties or additional costs based on kilometre limits.

Ability to Customize

When you finance and own a car, you can modify it to your heart’s content. Whether you want to enhance the interior, change the paint colour, or install new features, financing provides the freedom to make your car uniquely yours.

Financing a Car: The Cons

Although financing has its rewards, there are downsides to consider as well.

Higher Monthly Payments

Financing typically involves higher monthly payments than leasing since you’re paying for the full cost of the car. If you’re working within a tight budget, this aspect might be a challenge.

Depreciation

A major downside of financing is the depreciation of your car’s value over time. This can be frustrating, especially if you plan to sell the vehicle later and find that its resale value has significantly diminished.

However, buying a certified pre-owned vehicle or a car coming off a 2 to 3 year lease can save you a lot of money. These cars have already gone through the biggest drop in value, so you avoid the steepest part of the depreciation curve. You’ll typically pay only 60–70% of the price of a new car, while still getting a reliable vehicle—often with the original factory warranty still in place.

Maintenance Costs

Once the manufacturer’s warranty expires, you’ll be responsible for all maintenance and repair costs. This can add an extra layer of financial responsibility, especially for older vehicles.

Factors to Consider

How do you determine whether to lease or finance a car? Consider the following factors to make an informed, realistic decision.

Budget

Take a close look at your financial situation. Are you more comfortable with lower payments but ongoing costs (leasing), or are you willing to commit to a higher cost upfront to eventually own the car (financing)? Understanding what fits your budget will help narrow down your options.

Driving Habits

Do you have predictable driving patterns, or do you frequently travel long distances? If mileage restrictions would be a problem, financing is likely the better choice.

Long-Term Plans

Think about your long-term goals. Are you looking for a short-term commitment or a long-term investment? If you’re planning to purchase a car for tax purposes or want to keep it for years to come, financing might align better with your vision.

Depreciation vs. Convenience

Consider how much you value convenience versus asset building. Leasing reduces upfront costs and maintenance concerns but doesn’t allow you to build equity. Financing, on the other hand, offers ownership at a higher initial cost.

Credit-Building Opportunities

Both leasing and financing a car can help you build credit, but the impact depends on how you manage your payments. With both options, timely payments are reported to credit bureaus, which can improve your credit score over time.

Leasing offers a structured payment plan, while financing demonstrates your ability to handle a larger, long-term debt. However, missed payments on either can negatively affect your credit, so consistency is key. Whether you lease or finance, a responsible payment history can go a long way toward establishing or strengthening your credit profile.

Make the Smart Choice for Your Lifestyle

Both leasing and financing have their unique advantages and drawbacks. Ultimately, the best choice depends on your personal situation, preferences, and financial goals. If you’re still unsure whether it’s smarter to lease or finance a car, our team at Blue Copper Capital can help. We offer personal loans tailored to fit your needs, making it easier to get behind the wheel on your terms. Contact us today to learn more about how we can support your car-buying journey.