When you need money fast, a payday loan can seem like the quickest way to get it. Before you sign anything, it helps to know exactly what the rules are, what lenders can charge, and what rights you have as a borrower. There are key protections built into Alberta’s lending laws, and knowing them means you can borrow with full clarity. Whether you’re exploring payday loan options for the first time or comparing products, it all starts with knowing your rights.

Alberta’s Consumer Protection Act sets clear limits on payday loan fees, loan amounts, and lender behaviour, giving you real protections every time you borrow. They’re how you can borrow with confidence and spot any lender that isn’t playing fair.

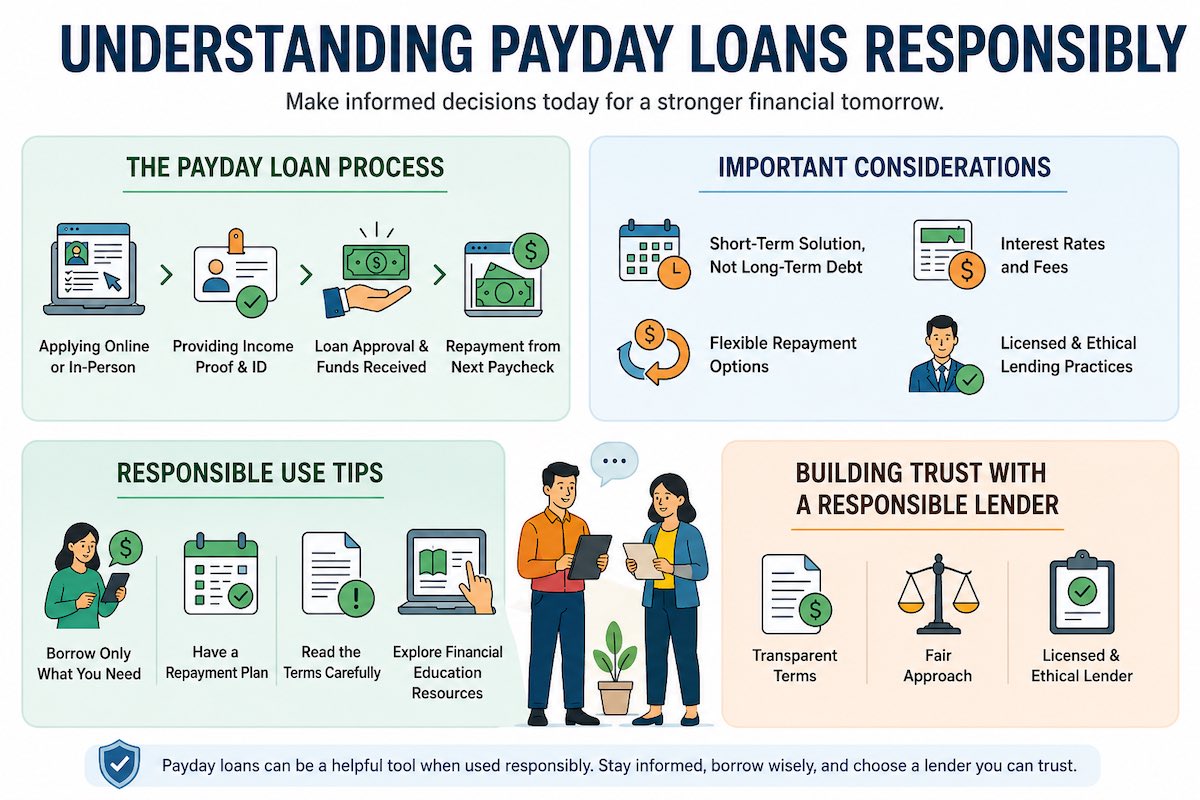

What Alberta’s Payday Loan Rules Actually Cover

Alberta’s payday loan laws exist to keep borrowing fair and transparent. The Consumer Protection Act governs every licensed lender in Alberta, which means the rules apply no matter where you go for a loan in the province. These laws cap fees, set limits on loan amounts, and define exactly how repayment works.

Any lender operating legally in Alberta has to follow these rules. If a lender can’t show you their licensing information or avoids answering questions about their fees, that’s a sign to look elsewhere.

Working with a licensed lender means you’re covered by these protections from the start.

How to Spot a Licensed & Responsible Lender

Checking a lender’s registration through Alberta’s government registry takes only a few minutes and provides a lot of information. A licensed lender won’t have any problem sharing that information with you. If they’re vague about it, move on.

Look for lenders who show you all fees upfront, don’t pressure you to apply quickly, and offer flexible loan options that match your situation. Strong signs of a responsible lender also include access to financial education resources so you fully understand your loan before committing. It’s also worth knowing when to say no to a loan and what red flags to watch for before you commit.

Here is what you should always look for in a trustworthy lender:

- Verify lender registration with Alberta’s government registry, especially for online lenders

- Look for clear, upfront fee disclosures

- No-pressure application process

- Flexible repayment options available

- Financial education is part of the conversation

A few other lender behaviours are specifically prohibited in Alberta. Lenders can’t practise “discounting,” which means deducting fees from your loan before giving you the money. If you’re approved for $300, you should receive the full $300, not $300 minus the fees. Lenders also can’t require you to buy another product or service as a condition of getting your loan. A payday loan has to stand on its own, without strings attached.

What to Watch for With Online Lenders

Alberta’s regulatory framework has reshaped the lending landscape over the past several years. Following the introduction of stricter lending rules in 2016, the number of licensed physical payday loan branches in Alberta dropped from about 220 to roughly 165 between 2016 and 2018. The lenders who couldn’t operate fairly under the new rules left the province, leaving a smaller, more accountable field of licensed providers.

The bigger risk today is online. While Alberta’s brick-and-mortar lenders are closely monitored, many online lenders operating in the province are unlicensed and don’t follow Alberta’s rules. The provincial government has flagged numerous unlicensed online lenders that ignore the $14 fee cap, charge higher rates, and use illegal collection tactics. Verifying a lender’s registration before applying, especially when borrowing online, helps you avoid getting caught in a bad situation.

Fee Limits & Cost Caps You Should Know

Under Alberta law, the maximum lenders can charge is $14 per $100 borrowed, which includes all fees and charges related to the loan. So if you take out a $300 payday loan, the most you should ever pay in fees is $42. You won’t face hidden charges within the base fee structure, though lenders can charge additional fees if the loan isn’t paid on time.

Payday loan amounts are also capped at $1,500 total. If you need more than that, a payday loan simply isn’t the right product for you. A lender can’t legally offer you more under this structure. These caps exist so you know exactly what you’re getting into before any money changes hands.

Alberta also sets rules on the length of your loan term. Payday loans must give you at least 42 days to repay, and no more than 62 days. This timeline is designed to give you enough room to repay without immediately needing another loan, which can start a cycle of debt that’s hard to break.

Rollover & Renewal Restrictions

Alberta law prohibits lenders from rolling over or extending your payday loan into a new one. A lender can’t keep renewing your loan and adding extra fees. A lender also cannot issue you a new payday loan while you still owe on a previous loan from them, which helps prevent overlapping debt from stacking up.

These rules exist to protect you from a cycle where a small loan grows into a much bigger problem.

Your Rights as a Borrower in Alberta

You have a 2-business-day window to cancel your payday loan after receiving a copy of your agreement, with no penalty. For example, if you sign on a Monday, you have until end of business Wednesday to walk away and return the borrowed amount at no extra cost. This cooling-off period gives you space to reconsider without pressure.

This right applies regardless of where you borrowed or how you applied. Whether you apply online, over the phone, or in person, the cancellation window remains exactly the same. If you cancel within the window, your lender is required to provide a receipt confirming the loan has been cancelled.

Repayment Rules That Protect You

Alberta’s payday loan rules also set clear expectations for how repayment works, so you aren’t caught off guard by penalties or unfair terms.

If you’re paid twice a month, every two weeks, or more often, your lender must offer you an installment plan that spreads your payments over at least three pay periods. This gives you more flexibility than paying back everything at once.

If a payment bounces, lenders cannot charge you more than $20 as an NSF (non-sufficient funds) fee. And if you fall behind on repayment, the overdue interest rate is capped at 30% per year. These limits exist to keep a short-term setback from turning into a financial spiral.

Required Disclosures Before You Sign

Before a lender releases any funds, they must show you the full cost of the loan in writing. This disclosure includes the total fees you’ll pay and the annual percentage rate (APR). The APR helps you compare the real cost of borrowing. Nothing should come as a surprise after you sign.

The law requires a written agreement before money moves. If a lender rushes you to accept funds before providing written terms, that’s a red flag you should take seriously.

Payday Loans vs. Personal Loan Alternatives

Payday loans meet small, short-term needs. They require a single repayment tied directly to your next paycheque. Personal loans often come with lower overall costs and longer repayment timelines, which can make monthly budgeting much easier.

Short-term loans through alternative lenders also tend to offer more flexibility in how you repay. Instead of one large lump-sum payment, you may be able to spread the cost over several weeks or months.

When a Personal Loan May Work Better for You

If you need more than $1,500, a payday loan legally can’t cover it. Quick cash loans through a personal loan product can offer higher amounts while still being structured and manageable. That flexibility really matters when you’re dealing with a larger unexpected expense.

Personal loans also work well when you want structured repayment instead of paying everything back at once. Work with a licensed, transparent lender so you can ask questions, review your options, and choose a repayment plan that fits your actual income and schedule. A skilled lender should be able to point you in the right direction.

Ready to Explore Your Options?

Understanding your rights and the laws protecting you is the first step toward making a smart financial choice. By knowing the rules around fees, renewals, and cancellations, you can take complete control of your borrowing experience and make the decision that best fits your budget.

Blue Copper Capital is a licensed lender offering personal loans, business loans, and payday loans in Calgary, Edmonton, and Vancouver with full transparency and no hidden fees. If you’re ready to find a practical solution, you can start your application online, call our team directly, or visit us in person to talk through what works best for you.